Potential Increases in Home Insurance Premiums Expected in 2025

As we look ahead, many property owners are pondering the financial landscape for safeguarding their cherished spaces. The dynamics affecting premiums are continually evolving, influenced by a variety of factors that can shift the balance between affordability and extensive coverage. Understanding these trends is crucial for anyone wanting to protect their assets without breaking the bank.

With natural disasters becoming more frequent and the economy experiencing fluctuations, there’s a growing curiosity about how these elements might impact the expenses associated with protecting residential properties. It’s natural to wonder if the costs involved in securing safety measures might escalate in the coming years.

In this discussion, we’ll delve into potential influences that could shape the costs of safeguarding your property. From environmental shifts to legislative changes, a multitude of elements could play a role in determining how much you might need to allocate for protection in the near future. Let’s explore the possibilities together.

Factors Influencing Home Protection Rates

When we talk about the costs associated with safeguarding your property, several elements come into play. These aspects can significantly affect how much you’ll need to budget for coverage, often causing fluctuations over time. Understanding these influences can help you navigate and even anticipate changes in pricing.

One major factor is the location of your residence. Areas prone to natural disasters, like floods or wildfires, often see higher premiums due to the increased risk of claims. Additionally, the local crime rate plays a vital role; properties in high-crime neighborhoods can have elevated costs to offset potential theft or vandalism.

The condition and age of your dwelling also matter. Older structures might require more repairs or are at greater risk for issues, making them more expensive to insure. Furthermore, features such as the type of roofing or plumbing systems can influence rates, as certain materials may be more resilient than others in the face of natural events.

Your personal history and choices contribute as well. A solid credit score can lead to better pricing, as insurers typically view it as a sign of responsibility. Moreover, the amount of coverage you select, including any additional riders or features, directly impacts the total cost.

Lastly, the overall state of the insurance market can shift due to economic conditions or regulatory changes, which may trickle down and affect individual policyholders. Being aware of these dynamics can empower you to make informed decisions regarding the protection of your asset.

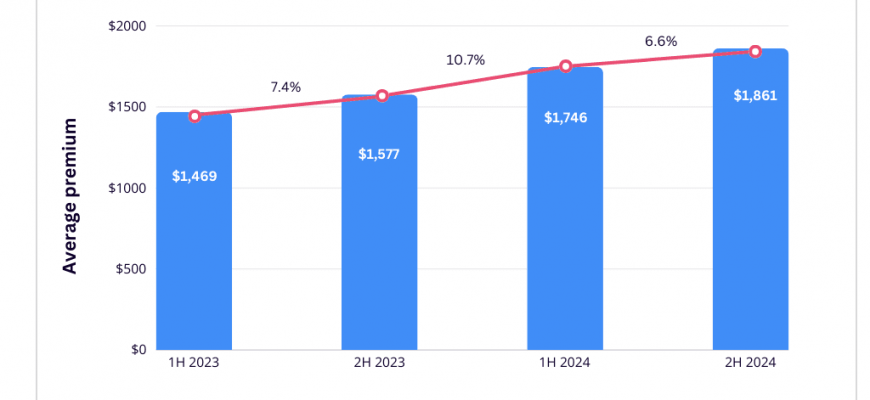

Predictions for Insurance Costs in 2025

As we look ahead, many are curious about the trajectory of coverage expenses in the upcoming years. Factors such as climate change, economic shifts, and technological advancements are all contributing to the evolving landscape of risk management services. Understanding these dynamics can provide valuable insights into potential financial implications for property holders.

The impact of extreme weather events has become increasingly prominent. Natural disasters can lead to higher claim rates, prompting companies to adjust their pricing structures. This may translate to elevated costs for policyholders, particularly in regions frequently affected by such occurrences.

Moreover, advancements in technology are altering how providers assess risk. Enhanced data analytics and IoT devices are becoming standard tools in evaluating properties and their vulnerabilities. As more precise assessments become the norm, this could lead to adjustments in premiums, reflecting the true level of risk associated with individual properties.

Beyond environmental factors, economic conditions play a vital role. Inflation rates, interest rates, and general market stability can all influence pricing strategies. A fluctuating economy may prompt companies to reassess their financial models, which could ultimately affect the amounts policyholders have to budget for.

Lastly, regulatory changes and industry competition can also shape future costs. New guidelines aimed at consumer protection or emerging competitors with innovative offerings might lead to a reshaping of existing pricing paradigms. As these elements converge, it’s essential for property owners to stay informed and proactive in managing their coverage options.

How to Prepare for Potential Increases

Anticipating possible hikes in coverage expenses can feel daunting, but a little preparation goes a long way. By taking proactive steps, you can better manage your finances and ensure that you’re ready for any changes that might come your way.

Start by reviewing your current policy. Understanding your existing coverage is crucial. Take note of the levels of protection you have, what it includes, and any areas where you might be over or under-insured. This knowledge will empower you to make informed adjustments if necessary.

Next, consider enhancing your property’s safety features. Simple upgrades, such as installing security systems, smoke detectors, or improved lighting, can not only protect your residence but might also lead to discounts in your premium. Investing in safety measures pays off in the long run.

It’s also wise to shop around and compare options. Different providers offer various prices and packages, so exploring your choices can pinpoint the best deal for your needs. Don’t hesitate to ask about possible discounts or bundles that can save you money.

Lastly, maintaining a healthy credit score can have a significant impact on your rates. Regularly monitor your credit report, and take steps to improve your score if needed. A better score often correlates with lower premiums, helping you to save more in the long term.