Understanding the Ideal Credit Score for Financial Success

When it comes to navigating the world of personal finance, there’s one aspect that often plays a critical role in your financial journey. This essential numeric representation acts as a key that can unlock various opportunities, be it securing a loan, renting a new apartment, or even landing your dream job. But what truly makes this numerical metric favorable, and how can you achieve an outstanding standing?

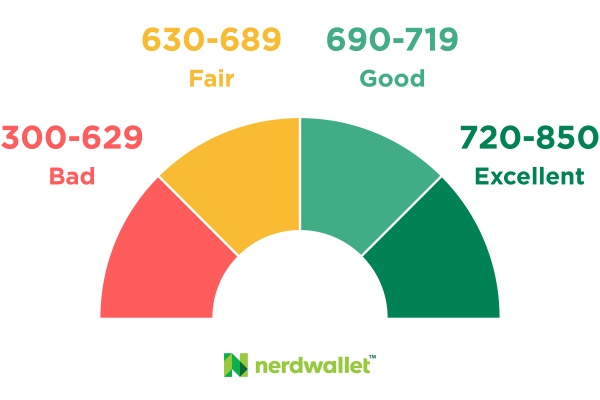

Understanding the intricacies of this numerical evaluation is fundamental. Many individuals are uncertain about what number they should aim for to achieve favorable conditions in financial dealings. It’s not just about a single digit; it encompasses various elements that reflect your fiscal responsibility and overall financial well-being. Grasping the significance of high-performance metrics can set the foundation for a secure financial future.

Throughout this discussion, we’ll explore the key components that contribute to a remarkable numeric evaluation. We’ll delve into strategies to enhance your standing and debunk common misconceptions that often cloud people’s understanding. By the end, you’ll feel empowered to take charge of your financial profile and work towards an impressive result.

The Importance of Financial Ratings

Understanding the significance of financial ratings can make a real difference in your life. These numerical values reflect your trustworthiness as a borrower, influencing various aspects of your financial journey. Whether you’re aiming to secure a loan for a dream home or to finance a new vehicle, having a solid numerical representation can open many doors for you.

One of the key roles of these ratings is in determining the interest rates you may be offered. A higher rating often translates to more favorable terms, meaning lower monthly payments. This can save you a substantial amount over time, allowing you to invest in other opportunities or enjoy more of life’s pleasures.

Beyond loans, your financial evaluation can impact other areas too. It may be a factor in securing rental agreements, getting a new job, or even obtaining insurance. Many companies check these ratings as part of their decision-making process, making it essential to maintain a good standing.

It’s also worth noting that having a strong financial rating can provide peace of mind. Knowing that you are viewed as a reliable borrower can give you confidence when tackling significant purchases or investments. Taking the time to understand and improve your financial standing can lead to a more stable and prosperous future.

Improving Your Financial Rating Effectively

Enhancing your financial reputation is more attainable than you might think. It requires a mix of strategy, patience, and a little discipline. By focusing on key areas, you can elevate your standing and open doors to better opportunities in the future.

Understand Your Report: The first step in making progress is to get familiar with your financial dossier. It’s a reflection of your borrowing history, and knowing what’s included will help you identify areas for improvement. Review it carefully and look for any discrepancies that may negatively impact your standing.

Timely Payments: One of the most crucial factors in this process is ensuring that you pay your bills on time. Establishing a habit of punctual payments can significantly boost your standing over time. Setting up reminders or automatic payments can help you stay on track.

Reduce Debt: Lowering your overall debt can also play a major role. Focus on paying down high-interest balances first, as this can free up your finances and reduce stress. Consider consolidating your debts if it provides a lower interest rate and more manageable payments.

Limit New Inquiries: Be mindful of how many new accounts you open within a short time span. Each application results in a hard inquiry, which can temporarily decrease your rating. Instead, space out your applications and think critically about whether you truly need that new account.

Maintain Old Accounts: Keeping older accounts open can help your overall standing as they contribute to your credit history’s length. Even if you’re not using them, they can show lenders your long-term reliability. Just ensure that you don’t miss payments on any of them.

Use Credit Responsibly: If you have credit cards, using them responsibly can demonstrate your ability to manage borrowing. Aim to utilize only a small percentage of your available limit each month. This shows potential lenders that you can handle credit well without maxing out your cards.

By applying these straightforward strategies, you’ll find that improving your financial reputation is a journey that can lead to better terms on loans, lower interest rates, and increased financial freedom in the long run.