Understanding the Significance of a High Credit Score and Its Impact on Financial Opportunities

In today’s world, a solid financial reputation can open many doors. It’s like a golden ticket that can lead to better opportunities, lower interest rates, and greater trust from lenders. A good standing in the financial realm is not just a number; it’s a reflection of responsibility and stability in managing one’s financial obligations.

When individuals pay attention to their financial habits and maintain a favorable standing, they set themselves up for success. It showcases their ability to handle loans, mortgages, and other forms of borrowing with care. This positive perception not only helps in securing loans but can also influence insurance premiums and rental applications. It’s essential to recognize the importance of maintaining an impressive rating and understanding the factors that contribute to it.

Many may wonder how this rating is determined and what steps can be taken to improve it. Various elements such as payment history, credit utilization, and the length of credit history play crucial roles. Being informed about these aspects empowers individuals to take charge of their financial lives, leading to better outcomes and opportunities in the long run.

Understanding the Importance of Credit Ratings

Having a solid evaluation of one’s financial behavior plays a crucial role in everyday life. It influences numerous aspects, from the ability to secure loans to the terms of those loans. A favorable assessment can often unlock better opportunities, allowing individuals to achieve their aspirations with less struggle.

Why does this matter? An excellent rating reflects responsibility and reliability, which lenders look for in potential borrowers. It can impact not just large purchases like homes and cars, but also daily necessities such as renting an apartment or even obtaining a mobile phone plan. In essence, it serves as a window into a person’s financial habits.

Monitoring your evaluation is essential for long-term financial health. Regular checks can help you understand where you stand and what actions you can take to improve your standing. By maintaining awareness, individuals can proactively manage their financial futures and avoid pitfalls that could lead to unfavorable outcomes.

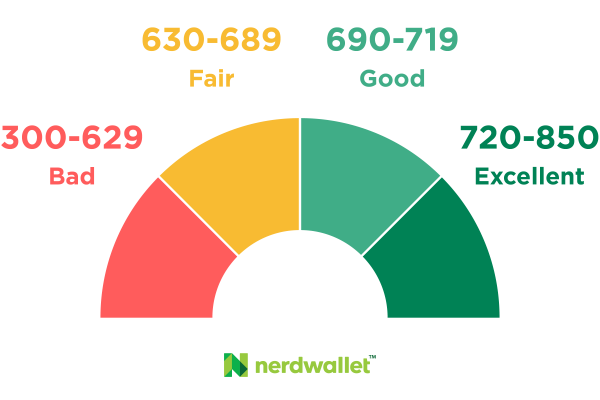

Factors Influencing Your Rating

Understanding the elements that can affect your financial evaluation is essential for anyone looking to improve their standing. Several key aspects play a significant role in determining how lenders view your financial behavior. By keeping these factors in mind, you can take proactive steps toward enhancing your overall assessment.

Payment History: One of the most critical components is your history of payments. Consistently paying bills on time shows lenders that you are responsible and reliable. Late payments, on the other hand, can create red flags and negatively impact your assessment.

Amounts Owed: The total amount of debt you currently have in relation to your available credit can influence your evaluation. It’s ideal to maintain a low balance compared to your limits. Keeping your utilization ratio low demonstrates that you can manage credit wisely.

Length of Credit History: The duration for which you’ve had credit accounts also matters. A longer credit history usually suggests stability and reliability, while a shorter one can make you appear more of a risk to potential lenders.

Types of Credit: Having a diverse array of credit types, such as credit cards, auto loans, or mortgages, may positively impact your overall standing. Lenders often prefer to see that you can handle different kinds of financial responsibilities.

New Credit: Frequent applications for new credit can be seen as a red flag. Each application triggers a hard inquiry, which can temporarily lower your rating. It’s wise to limit applications to what you truly need.

By being mindful of these elements, you can take charge of your financial reputation and work towards a more favorable evaluation in the eyes of lenders.

Benefits of Maintaining a Strong Financial Profile

Keeping an impressive financial rating can open doors to numerous advantages in your financial journey. Individuals who successfully manage their finances often enjoy a smoother experience when dealing with loans and other financial products.

Here are some key benefits of having a robust evaluation:

- Lower Interest Rates: A solid reputation often leads to reduced interest rates on loans and credit offerings, saving you money over time.

- Increased Approval Odds: Lenders are more likely to approve applications from those with an outstanding financial history.

- Better Negotiating Power: A strong financial profile gives you leverage when negotiating terms with lenders, potentially securing more favorable conditions.

- Easier Renting: Landlords often check financial ratings. A strong profile can make renting properties simpler and more affordable.

- Access to Premium Credit Products: Individuals with impressive profiles may qualify for exclusive credit cards and rewards programs that offer better benefits.

By prioritizing your financial health, you can enjoy these advantages and create a more secure financial future. It’s all about making informed decisions and maintaining responsible habits!