Understanding Unsubsidized Loans in Financial Aid Programs

When it comes to pursuing higher education, many individuals find themselves exploring various financing methods to cover their costs. One option that often comes into play is a certain type of borrowing that doesn’t come with the same benefits as other forms of support. This choice can be vital for students who require extra funds but may not qualify for all the advantages that some programs offer.

In essence, this borrowing method allows students to access funds without the government covering interest while they are enrolled. As the expenses climb higher, it’s important to grasp how this option works and what implications it carries for your future repayment obligations. By understanding the specifics, you can make informed decisions that align with your educational and financial goals.

Embracing this pathway involves recognizing both the advantages and the responsibilities that accompany it. It’s essential to weigh your choices carefully, ensuring that you are prepared for the commitment that comes with borrowing. Knowledge is power, and being well-informed can set you on the right course towards achieving your academic dreams.

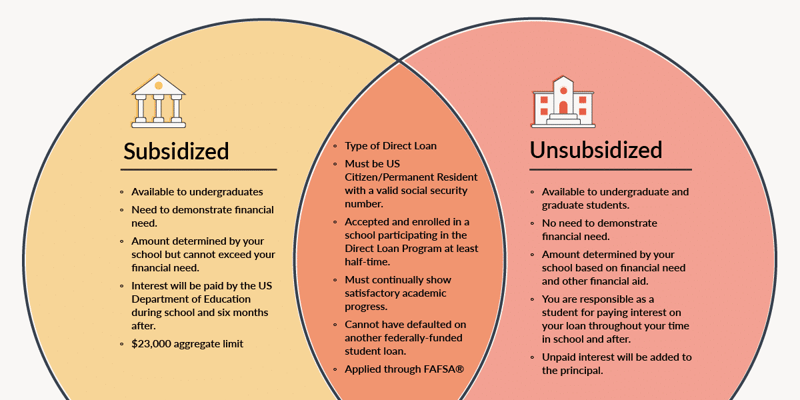

Understanding Unsubsidized Student Loans

When it comes to financing your education, there are various options out there, each with its own nuances. One type that often comes up is the kind of assistance where interest begins to accrue right from the moment the funds are disbursed. This means that while you’re focusing on your studies, the amount you owe can steadily increase.

Let’s break it down a bit:

- Interest Accumulation: Unlike some other options, you’re responsible for all the interest accruing while you’re in school. This can add up quickly, so it’s essential to keep track.

- Flexible Amounts: You can typically borrow a certain amount each academic year, which may vary based on your educational status and expenses.

- No Credit Requirements: Generally, there are no credit checks involved, making it accessible for many individuals who might struggle to find other forms of assistance.

It’s important to understand that responsibilities attached to these funds can impact your financial future, especially upon graduation. Here are a few tips to keep in mind:

- Consider Interest Payments: If possible, make occasional payments on the interest to help reduce the overall burden.

- Budget Wisely: Plan ahead for repayments and factor this into your post-graduation financial strategy.

- Stay Informed: Regularly check your statements and stay aware of how much you owe and the interest rates applicable.

In summary, understanding this type of assistance is crucial for navigating your educational financing options and ensuring you make informed decisions as you pursue your goals.

Key Features of Financial Support Options

When exploring options for educational funding, it’s essential to understand the primary characteristics of various types of support. Each type offers unique terms and benefits that can significantly influence your financial journey through school. Knowing these features can help you make informed decisions and manage your educational expenses effectively.

One of the major aspects to consider is interest accumulation. Unlike some other forms of support, interest on these options begins to accrue immediately after the funds are disbursed. This means that while you’re focused on your studies, your balance may grow, affecting the total amount you owe once repayment starts.

Additionally, these options often have flexible eligibility criteria, making them accessible to a wide range of students. Requirements typically depend on factors such as enrollment status, financial circumstance, and credit history. This flexibility can be a significant advantage for those seeking assistance in covering tuition and related expenses.

Another key feature is the repayment timeline. Borrowers usually have a grace period after graduation or dropping below half-time enrollment before they must start repaying the borrowed funds. This can provide a helpful transition into post-college life, allowing time to secure employment and manage other financial responsibilities.

Lastly, the potential for various repayment plans can be highly beneficial. Many options offer different methods for managing repayments, accommodating various financial situations. Understanding these can empower you to choose the plan that fits your circumstances best, helping you maintain control over your finances post-education.

Repayment Options and Considerations

When it comes to paying back borrowed funds, there are several paths you can take. It’s essential to understand the choices available to ensure you make the best decision for your personal situation. Different repayment plans can cater to varying financial circumstances, allowing some flexibility in how you manage your finances once your studies are complete.

One common route is the standard repayment plan, where you pay a fixed amount each month over a specified period. This option is straightforward and allows you to clear your balance relatively quickly. However, if your finances are tight, you might consider an income-driven plan, which adjusts your monthly payments based on your earnings, potentially offering much-needed relief during times of financial strain.

Another important aspect to consider is the interest that accrues while you’re in school, which can impact the total amount you’ll ultimately pay back. Keeping track of this can help you strategize your payments post-graduation. Additionally, some individuals find consolidation or refinancing beneficial, as it can simplify their payment process and possibly lower interest rates.

Finally, staying informed about different repayment options and making timely payments is crucial in avoiding default. Engaging with your lender and asking questions can lead to finding the best solution tailored to your needs. Remember, planning ahead is key to managing your obligations effectively and ensuring financial stability in the long run.