Exploring the Concept of Credit Grades and Their Importance in Financial Decision-Making

In the world of finance, it’s essential to gauge the likelihood of an individual or entity to meet its obligations. This evaluation not only influences lending decisions but also significantly impacts the terms of borrowing and interest rates. It’s like a report card for managing money, providing insight into reliability and responsibility, which are key factors in any financial transaction.

These assessments play a crucial role in the economy, guiding both lenders and borrowers in making informed decisions. Just as a student’s performance is measured through evaluations, individuals and businesses are similarly rated based on their financial behaviors and history. The nuances of these scores can often dictate access to funds, shaping the journey of personal finances or business ventures.

Understanding these evaluations is vital for anyone looking to navigate the financial landscape effectively. Knowing how these ratings are determined and what they signify can empower individuals and organizations to improve their standing and make wiser financial choices. Let’s delve into the intricacies of this fascinating aspect of finance and uncover what it all means for you.

Understanding Ratings and Their Importance

In the world of finance, certain indicators play a critical role in assessing an individual’s or organization’s financial reliability. These markers help lenders and investors make informed decisions about whether to extend loans or investment opportunities. Grasping the nuances of these ratings is essential for anyone looking to navigate the economic landscape effectively.

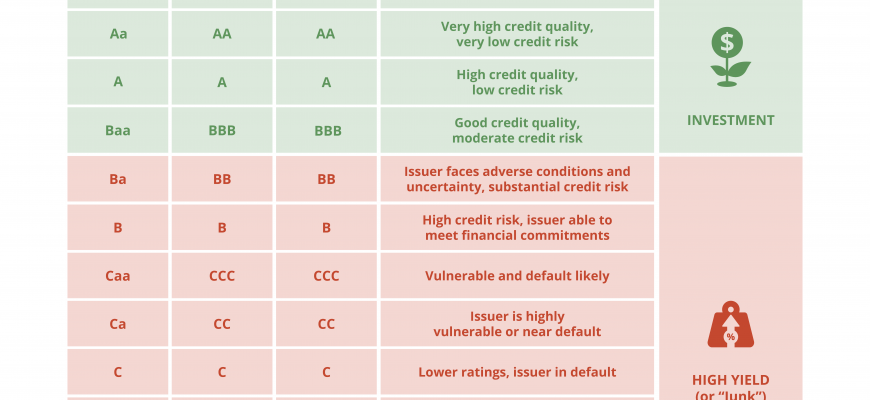

Ratings serve as a summary of an entity’s financial behavior and trustworthiness. They reflect how responsibly one manages debt and other obligations. A high score often signifies a history of timely payments and sound financial practices, which in turn opens doors to better borrowing options and lower interest rates. Conversely, a lower score may lead to onerous terms or even denial of credit altogether.

It’s vital to recognize the various factors that contribute to these evaluations. Elements such as payment history, outstanding debt, duration of credit relationships, and types of credit utilized all play a role. By understanding how these components interact, individuals can take proactive steps to improve their standing in the eyes of lenders.

Additionally, these assessments have wider implications beyond personal finance. Businesses also rely deeply on ratings to attract investment and secure favorable terms from banks. A solid rating can enhance a company’s credibility and facilitate growth opportunities.

In summary, familiarity with these ratings empowers consumers and businesses alike to make smarter financial choices. Being aware of how one’s financial habits affect these scores can lead to better management and a brighter economic future.

Factors Influencing Your Rating

Many elements come into play when determining your standing in the financial world. Understanding these aspects can empower you to make informed decisions and potentially improve your position over time. It’s essential to recognize how different behaviors and circumstances can affect the perception lenders have of you.

Your payment history is one of the most crucial factors. Regular and timely payments signal reliability, while late payments or defaults can seriously harm your reputation. Additionally, the total amount of debt you carry relative to your available credit limits plays a significant role. This balance reflects your ability to manage financial obligations responsibly.

The length of your credit history also contributes to your overall assessment. A longer track record can illustrate a stable financial behavior, whereas a brief history may leave lenders with questions about your reliability. Furthermore, the types of accounts you hold–ranging from installment loans to revolving credit–offer insight into your ability to handle different forms of debt.

Lastly, frequent inquiries about your financial status can raise red flags. While it’s normal to shop around for better terms, excessive probing may signal financial instability. Keeping these factors in mind can help you navigate the complex landscape of financial assessment and strive for a more favorable position.

How to Improve Your Score

Enhancing your financial standing is a journey that requires a bit of effort and understanding. It’s about making conscious decisions and adopting habits that promote better financial health. Many factors contribute to this overall rating, and knowing how to navigate these elements can truly make a difference.

Start by regularly checking your reports for inaccuracies. Mistakes happen, and spotting them early can lead to corrections that boost your standing. Don’t hesitate to reach out to relevant agencies to dispute any errors you find. It’s a vital step towards improving your overall picture.

Additionally, maintain a consistent payment history. Making payments on time is essential; even one missed payment can negatively affect your evaluation. Setting up automatic payments or reminders can help keep you on track and avoid these pitfalls.

Utilizing a manageable portion of your available credit is another key factor. Aim to keep your usage below 30% of your limit. This practice signals to potential lenders that you are responsible and not over-relying on borrowing options.

Finally, while it might seem tempting, refrain from opening too many new accounts in a short time. Each application generates a hard inquiry, which can temporarily lower your rating. Instead, focus on cultivating and maintaining existing accounts. This strategy will contribute positively in the long run.