Understanding the Significance of Credit Scores and Their Impact on Your Financial Health

Understanding the various aspects of personal finance can often feel overwhelming, especially when it comes to those intriguing little numbers that seem to hold so much weight in our financial lives. These ratings play a crucial role in determining how lenders perceive an individual’s financial reliability. They essentially act as a snapshot of someone’s creditworthiness, influencing major decisions like loan approvals and interest rates.

In a world where financial interactions are becoming increasingly digital, grasping the essence of these assessments is essential. They not only reflect past financial behaviors but also shape future opportunities. Consequently, maintaining a positive standing in this area can open doors to better financial products and services, which is something many people aspire to achieve.

Delving deeper into the intricacies of these numerical representations provides insight into their impact on our daily lives. Regular monitoring and understanding of one’s standing can empower individuals, enabling smarter financial choices. After all, knowledge is power, especially when it involves navigating the complex landscape of personal finance.

Understanding the Fundamentals of Credit Scores

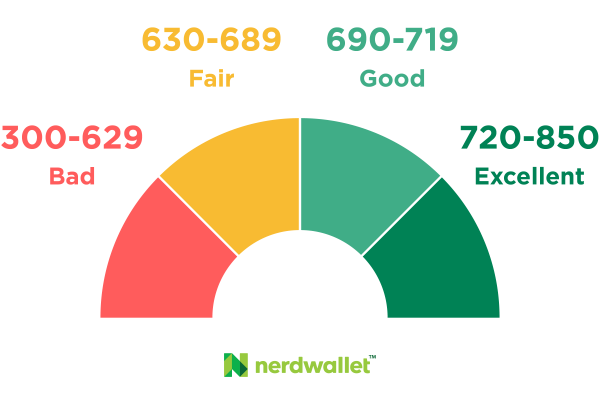

When it comes to personal finance, a particular number can play a crucial role in determining your borrowing potential and overall financial health. This figure reflects your creditworthiness and can influence a wide array of financial decisions throughout your life.

So, what are the essential aspects to grasp?

- Evaluation of Financial Behavior: This number is calculated based on your historical financial activities, including loan repayment habits, the amount of debt you carry, and the length of your credit history.

- Factors Influencing the Value: Several elements contribute to this metric. Key factors include payment history, amounts owed, length of credit history, types of credit accounts, and new credit inquiries.

- Importance for Lenders: Financial institutions often rely on this number to assess risk before approving loans. A higher figure typically leads to better interest rates and terms.

Understanding these basics can empower you to make informed decisions about your financial future. Here’s a quick overview of how you can take control:

- Regularly monitor your financial reports to stay informed.

- Maintain timely payments to boost your rating.

- Diversify types of credit to enhance your profile.

By grasping these fundamentals, you’ll be better equipped to navigate the intriguing world of personal finance and utilize this key element to your advantage.

The Impact of Credit Ratings on Loans

Understanding how financial ratings influence borrowing options is crucial for anyone looking to secure funding. These ratings play a significant role in determining not just whether a lender will approve an application, but also the terms that come with the loan.

Lenders rely on these assessments to evaluate the risk associated with a potential borrower. A high rating often translates to lower interest rates, making repayment more manageable, while a lower rating may lead to higher costs or even denial of the application. This dynamic can greatly affect a person’s financial landscape and future plans.

Additionally, your financial reputation can sway the types of loans accessible to you. For instance, someone with a robust rating might qualify for premium options, such as personal loans with favorable conditions, while those with weaker ratings may be limited to secured loans, requiring collateral to mitigate risk.

The implications are far-reaching; not only do financial ratings influence borrowing capability, but they also impact other areas like insurance premiums and rental agreements. Maintaining a positive rating can provide significant advantages and open doors in various financial aspects.

Improving Your Credit Score: Tips and Strategies

Enhancing your financial standing can feel like a daunting task, but there are practical steps you can take to boost your standing. By understanding the important factors at play, you’ll empower yourself to make better decisions that will reflect positively on your overall financial health.

One of the first things you can do is to consistently pay your bills on time. Establishing a reliable payment history showcases your accountability and reliability as a borrower. Setting reminders or automating payments can help ensure you’re never late.

Another key strategy involves keeping your balance levels low on revolving accounts. Aim to use less than 30% of your available credit at any given time. This not only shows that you’re not overly reliant on borrowed funds but also helps maintain a favorable ratio that lenders often evaluate.

Regularly reviewing your financial report is essential. Errors can occur, and having inaccuracies on your report could negatively impact your standing. If you spot any discrepancies, don’t hesitate to dispute them promptly.

Building a diverse portfolio of credit types can also be beneficial. A mix of installment loans, credit cards, or even retail accounts can demonstrate your ability to manage different kinds of debt responsibly. Just ensure that you don’t take on more than you can handle, as this could backfire.

Finally, consider becoming an authorized user on a trusted peer’s account. If they maintain a positive history, it may reflect well on you without the responsibility of managing the account entirely. Just be mindful that their actions could affect your standing as well.