Understanding the Differences Between Credit Notes and Refunds

When it comes to transactions, customers may encounter various ways to rectify issues like overpayments or returned goods. It’s essential to understand the different methods businesses use to address these situations and how they impact our finances. One of the common terms that might pop up in these scenarios often raises questions about its true nature and purpose.

You might be familiar with a situation where a merchant issues a document to acknowledge a financial adjustment rather than returning cash directly. This process can sometimes lead to confusion, especially when trying to establish whether it equates to simply getting money back or if it operates under a different principle altogether. Are we genuinely being compensated for our loss, or is it merely a shifting of values within the accounts?

Diving deeper into this topic can uncover distinctions that clarify our understanding of these financial transactions. Grasping the nuances between monetary return and adjustment is vital for anyone looking to manage their economic interactions effectively. So, let’s explore whether this form of transaction resembles getting your hard-earned cash back or if it serves a distinct function in the business world.

Understanding the Concept of Credit Notes

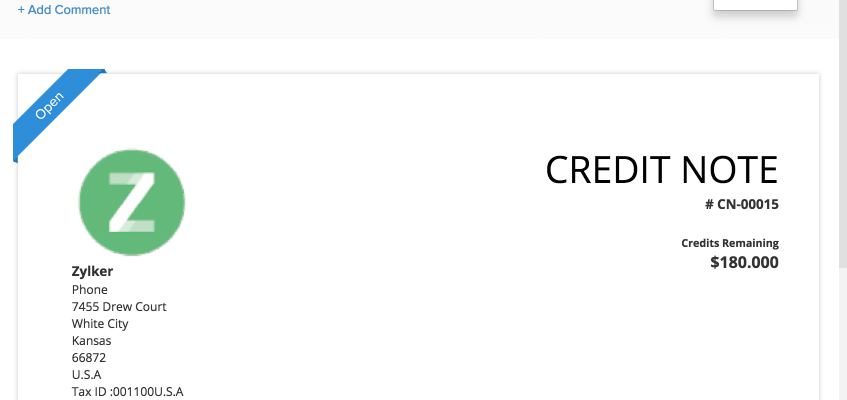

In the world of transactions, there’s a fascinating mechanism that allows businesses to manage adjustments and maintain customer satisfaction. This tool is essential for handling discrepancies, whether it’s a return, an overcharge, or simply a customer needing to alter their purchase. By grasping how this system operates, both sellers and buyers can navigate the financial landscape more confidently.

Essentially, this mechanism serves as a formal record acknowledging that a particular amount has been set aside for the customer due to a specific reason. It provides the option to either apply this sum towards future purchases or receive a different form of financial adjustment. This approach not only helps in maintaining accurate financial records but also fosters goodwill between parties, ensuring that customer relations remain strong even when issues arise.

To put it simply, this system is like a promise from the seller to the buyer, assuring them that their concerns are taken seriously. It creates a sense of trust and encourages ongoing engagement. When utilized correctly, this tool can be a win-win for everyone involved, as it offers a straightforward solution to potential conflicts while keeping the overall shopping experience positive.

The Difference Between Refunds and Credit Notes

When it comes to managing transactions, understanding the distinctions between various financial adjustments is crucial. Often, people use terms interchangeably, but they represent different processes and implications for consumers and businesses alike. Knowing how these mechanisms operate can help clarify expectations and ensure smoother interactions between customers and sellers.

One primary distinction lies in how value is represented. A reimbursement typically involves returning money directly to the purchaser’s account, essentially reversing the initial payment. In contrast, an alternative method of value adjustment provides a form of store credit or future purchasing power, allowing the buyer to use it for future transactions at that establishment.

Each approach serves unique purposes and satisfies different needs. The direct cash reimbursement is often preferred for its immediacy and simplicity. On the other hand, the alternative form encourages ongoing customer loyalty by incentivizing future buying, keeping the relationship between the business and client active.

Ultimately, the choice between these options depends on the context and preferences of the involved parties. Recognizing the differences can lead to more informed decisions and enhance the overall shopping experience.

When to Use a Credit Note in Transactions

In the realm of business dealings, there are times when adjustments need to be made to previous transactions. This is where an alternative financial document comes into play, serving as a formal acknowledgment of an alteration in the original sale. Such instances arise due to various reasons, and knowing when to implement this type of document can streamline processes and maintain positive relationships with customers.

You might find yourself in a situation where a buyer returns a product due to defects or dissatisfaction. Instead of merely processing an outright money return, issuing this document can provide a flexible solution, allowing the customer to use the associated value for future purchases. This not only keeps the funds within your business but also encourages ongoing patronage.

Additionally, if there are pricing discrepancies or discounts that weren’t initially accounted for, adjusting the financial records with such a document can rectify the situation smoothly. It essentially revises the transaction to reflect the correct amounts, ensuring clarity and transparency on both sides.

Another scenario could involve providing compensation for service issues or delays. Instead of a direct money return, granting an amount through this financial instrument can safeguard your cash flow while offering the customer a sense of resolution.

Recognizing when to utilize this type of documentation is crucial for maintaining a balanced approach to customer service and financial management. Whether dealing with returned items, billing errors, or service failures, it provides a means to address situations thoughtfully and professionally.

She’s an absolute vision of elegance and charm! Every second of this video is breathtaking. I can’t stop watching—it’s that captivating!