Understanding the Factors That Determine How Much Your Credit Score Can Decrease

Ever wondered how your financial appraisal can fluctuate based on your actions? It’s a topic that often sparks curiosity and concern among individuals keen on maintaining their financial health. In today’s world, where every decision can have far-reaching effects, understanding the factors that influence our financial ratings is crucial.

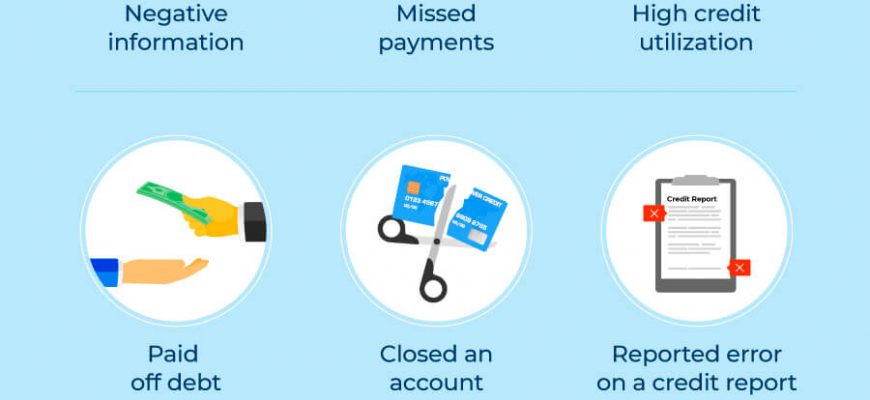

Many people might be surprised to learn just how sensitive these evaluations can be. Various circumstances, from missed payments to new inquiries, can lead to shifts that may feel quite significant. It’s essential to grasp not only the reasons behind these changes but also their potential implications for your financial future.

As we delve into this subject, we’ll explore the common triggers that can lead to a decline in your financial evaluation. By arming yourself with knowledge, you can make informed decisions that will help you navigate the complex world of finance with confidence and ease.

Understanding Factors Affecting Credit Scores

When it comes to evaluating your financial health, various elements come into play. These components can influence how lenders view your reliability and overall financial behavior. Grasping these aspects is crucial for anyone wanting to maintain a solid profile in the eyes of potential creditors.

Your financial history isn’t just about what you’ve borrowed; it encompasses your payment habits, the duration of your accounts, and even how much credit you’ve utilized. Each detail paints a picture of your management skills and trustworthiness, which can shift over time based on your actions.

If you’re wondering why certain behaviors might lead to a drop in your overall financial rating, consider aspects such as timely payments and the variety of your credit accounts. Even the number of inquiries made into your financial record can play a role. Understanding these nuances can help you navigate better financial decisions and hopefully steer clear of setbacks.

Impact of Late Payments on Credit Ratings

Delays in settling obligations can have a significant effect on financial profiles. When payments are not made on time, it can create a ripple effect that influences how lenders perceive an individual’s reliability. Understanding this impact can be crucial for anyone looking to maintain or improve their financial standing.

When payments are missed, financial institutions may report these incidents to agencies that track such behaviors. This information often becomes part of an individual’s financial history, potentially leading to decreased trust from lenders. The severity of the decline may vary based on how late the payments are and how frequently these occurrences happen.

Timeliness plays a key role in maintaining a positive financial image. Even a single late payment can lead to repercussions, particularly if it exceeds a certain duration. Early stages of lateness may trigger warnings, while more significant delays can lead to lasting damage. Lenders may view individuals with a history of missed payments as risky candidates for future loans.

Keeping track of due dates and setting reminders can help avoid these pitfalls. Building a habit of punctuality not only fosters better financial health but also supports a more favorable view from potential creditors. In the end, staying on top of payments can be a simple yet effective way to ensure a bright financial future.

Influence of Utilization on Financial Ratings

Maintaining a healthy relationship with available funds plays a crucial role in determining one’s overall financial assessment. It’s all about how well you manage the resources at your disposal. Proper handling can lead to positive reflections on your financial reputation, while mismanagement may lead to undesirable effects.

A significant factor affecting this rating is utilization, which refers to the ratio of used funds to the total available limit. It’s important to keep this percentage sensible to foster a better assessment. Here are some insights on why this matters:

- Balanced Approach: Staying within a reasonable limit shows lenders that you know how to manage your finances responsibly.

- Lower Ratios: Aiming for a utilization rate below 30% is generally deemed favorable. It signals to potential creditors that you’re not overly reliant on borrowed money.

- Impact of High Usage: If your utilization rate exceeds recommended levels, it could trigger alarm bells for lenders, portraying you as a higher-risk borrower.

In summary, effective management of available resources can significantly enhance your financial standing. Maintaining a low utilization rate can open doors to better opportunities, while high usage may lead to difficulties in securing favorable terms. By being aware of these dynamics, individuals can make informed choices that positively impact their financial journeys.