Understanding the Factors That Can Lead to a Decrease in Your Credit Score

Many individuals find themselves puzzled when they notice a decrease in their financial evaluation. It’s a concern that often warrants investigation, especially when your purchasing power and loan eligibility are at stake. There are various factors at play that can contribute to a less favorable assessment, and recognizing these can pave the way for better financial health.

The truth is, life is full of financial decisions that can impact this all-important figure. From late payments to increased utilization of available funds, understanding these elements is crucial. By being aware of what might affect that evaluation, you can make informed choices that support a more beneficial financial future.

In this discussion, we’ll explore the common pitfalls that lead to a less favorable assessment. Armed with this knowledge, you’ll gain insights into how to protect and nurture your financial standing, ensuring you remain in good shape when it comes to borrowing and lending. Let’s dive into the aspects that might be silently working against you.

Common Factors That Lower Your Score

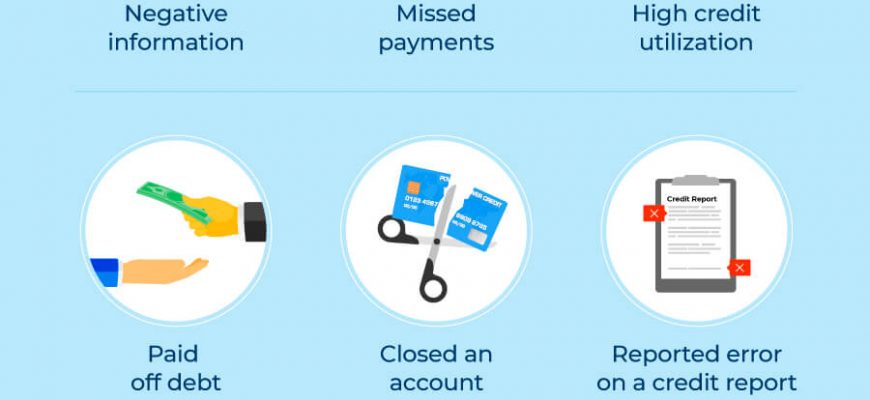

Many aspects can negatively impact the numerical representation of your financial trustworthiness. Understanding these elements can help you navigate your financial journey more effectively. Let’s dive into some common reasons that might lead to a less favorable evaluation of your financial behavior.

Missed Payments can significantly tarnish your reputation. When bills are unpaid or overdue, it raises red flags, signaling financial irresponsibility to potential lenders.

High Credit Utilization is another critical factor. If you consistently use a large portion of your available credit, it suggests that you might be over-relying on borrowed funds, which can be seen as risky behavior.

Account Inquiries also play a role. Each time you apply for new credit, lenders perform a hard inquiry. Too many of these requests within a short time frame can imply desperation for funds, which is not an attractive quality in a borrower.

Length of Credit History matters as well. If you’re relatively new to the borrowing scene, your limited experience can result in a lower assessment. A longer, well-managed history tends to work in your favor.

Defaults or Bankruptcies are severe blemishes on your financial record. These situations are regarded very seriously and can remain on your profile for years, significantly hindering your appeal to lenders.

By keeping a close eye on these factors, you can maintain a healthier financial standing, ultimately leading to more opportunities when it comes to borrowing and financial growth.

Impact of Late Payments on Credit

Making payments on time is crucial for maintaining financial health. When payments are delayed, it can trigger a series of negative consequences that affect your financial profile. This section dives into the various ways overdue payments can influence and alter your financial standing.

First and foremost, late payments can lead to significant penalties and interest hikes. Most lenders impose fees for overdue amounts, which accumulate over time. This not only increases the amount owed but can also create a vicious cycle of missed payments and growing debt.

Furthermore, the impact extends beyond immediate financial repercussions. Many lending institutions report delayed payments to credit bureaus, which can tarnish one’s financial reputation. Even a single late payment can linger on records for several years, influencing future borrowing potential.

Additionally, frequent tardiness may indicate to potential lenders a lack of responsibility with finances, making it challenging to secure favorable loan terms. When trust is eroded, interest rates may rise, leading to more costly borrowing options.

Maintaining good payment habits is essential for long-term financial stability. Strategies like setting up reminders or automatic payments can help ensure obligations are met promptly, therefore shielding against the adverse effects that delays can bring.

Impact of Debt Utilization on Ratings

When it comes to evaluating financial trustworthiness, one key factor plays a significant role: the balance between available credit and outstanding debt. This ratio not only serves as a reflection of a person’s financial habits but also influences how lenders perceive their reliability. Striking the right balance is essential to maintain a favorable standing in the eyes of financial institutions.

Carrying high levels of debt relative to what you can borrow often sends a red flag to lenders. It suggests potential risks and raises concerns about the ability to manage financial responsibilities effectively. Keeping this ratio in check is vital; ideally, it’s best to keep outstanding balances below a certain threshold to appear more appealing to potential creditors.

Regularly monitoring this aspect can lead to healthier financial outcomes. Making a conscious effort to reduce outstanding balances or increase available credit can help improve that all-important ratio. Ultimately, understanding and managing debt utilization is crucial for anyone looking to enhance their financial profile and unlock better opportunities in the future.