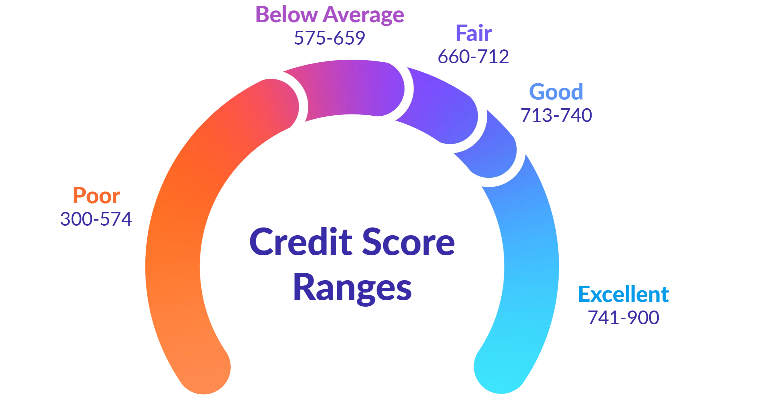

Understanding the Mechanics of a Credit Score and Its Impact on Your Financial Life

In the realm of personal finance, one concept often arises that plays a pivotal role in determining financial opportunities. This concept acts like a numerical representation of an individual’s trustworthiness when it comes to borrowing. It influences various aspects of life, from securing loans to renting homes, and even impacting insurance premiums. Knowing more about this system can empower individuals to make informed choices about their financial future.

Essentially, it encapsulates a few critical elements of your financial behavior, reflecting how you manage your obligations. This numerical figure is calculated based on your history, showing creditors how responsible you’ve been with managing debts and fulfilling commitments. Understanding its intricacies can reveal pathways to boosting your financial standing and unlocking better financing options.

Many people might wonder what factors really shape this numerical value. Various components come into play, including payment history, amounts owed, and the length of credit history. Grasping the nuances of these elements equips you with the knowledge needed to navigate through the financial landscape effectively. By deciphering how this system functions, you can take proactive steps toward enhancing your financial health.

Understanding Credit Score Mechanics

Let’s dive into the intricacies behind those elusive numbers that reflect your financial reliability. These ratings are not just random figures; they are constructed from various elements that come together to represent how trustworthy you are as a borrower. Grasping these components can empower you to manage your financial health more effectively.

One of the primary factors that influences this numeric representation is your payment history. Consistent payments signal responsibility and reliability. Next up is the amount owed, which considers how much of your available credit you’re currently utilizing. Keeping balances low relative to your limits is key here. Additionally, the length of your credit journey plays a role–established histories can indicate stability.

A piece of this puzzle also includes the types of credit accounts you possess. Diverse forms, like revolving and installment accounts, can enhance your standing. Finally, too many inquiries into your financial status within a short period can negatively impact your reputation. Staying informed about these elements is crucial for maintaining a healthy standing in the financial world and achieving your goals.

Factors Influencing Your Credit Rating

Your numerical representation of financial trustworthiness is shaped by several key elements. Understanding these components can help you manage your financial reputation more effectively and work towards enhancing it over time.

Payment History: One of the most significant factors is your record of on-time payments. Late payments, defaults, or any delinquencies can negatively impact your standing. Consistency in meeting obligations showcases reliability to lenders.

Credit Utilization: This refers to the ratio of your current debt to your available credit. Keeping this percentage low indicates that you use credit responsibly. Ideally, staying below 30% is considered favorable.

Length of Credit History: The duration over which you have managed credit plays a role as well. A longer credit history often suggests a proven ability to handle financial commitments. However, newcomers can still build a positive profile over time.

Types of Credit: A diverse mix of credit accounts–such as revolving accounts, installment loans, and retail accounts–can reflect your versatility in managing different financial products. Lenders often prefer to see a well-rounded profile rather than reliance on just one type of credit.

Recent Inquiries: Whenever you apply for new lines of credit, a hard inquiry is made, which can slightly lower your rating temporarily. Too many inquiries within a short period may signal risk to lenders, so it’s wise to space out applications.

By focusing on these aspects, you can work towards optimizing your standing in the financial landscape. Regular reviews of your financial habits will further support your journey to achieving a strong reputation.

Impact of Financial Ratings on Personal Wealth

Understanding how financial assessments influence your monetary journey can be a game-changer. These ratings play a pivotal role in shaping lending opportunities, insurance premiums, and even rental agreements. It’s fascinating to see how a numerical value can open or close doors in various aspects of life.

When it comes to securing loans, individuals with higher assessments typically enjoy lower interest rates. This leads to substantial savings over time, especially for long-term commitments like mortgages. Lenders perceive those with solid ratings as less risky, which often translates into better financial terms.

In addition to loan applications, financial ratings can affect insurance costs. Many providers review these assessments to gauge the risk level of potential clients, which can result in varied premium rates. A favorable rating can lead to significant savings in insurance expenditures.

Even in the realm of renting a property, landlords frequently evaluate these numbers to filter prospective tenants. A strong rating can give you a competitive edge, making it easier to secure a desirable living space without the hassle of hefty deposits or co-signers.

In essence, monitoring and improving your financial assessment can profoundly impact multiple areas of your financial existence. Taking proactive steps to ensure a healthy rating can promote better economic opportunities and enhance overall financial stability.