Understanding the Mechanics Behind Credit Scores and Their Impact on Financial Health

Navigating the world of finances can feel overwhelming at times, especially when it comes to assessing how individuals manage their monetary responsibilities. This system often plays a crucial role in determining eligibility for loans, mortgages, and even rental agreements. It’s fascinating how a seemingly simple calculation can have such a profound impact on one’s economic opportunities.

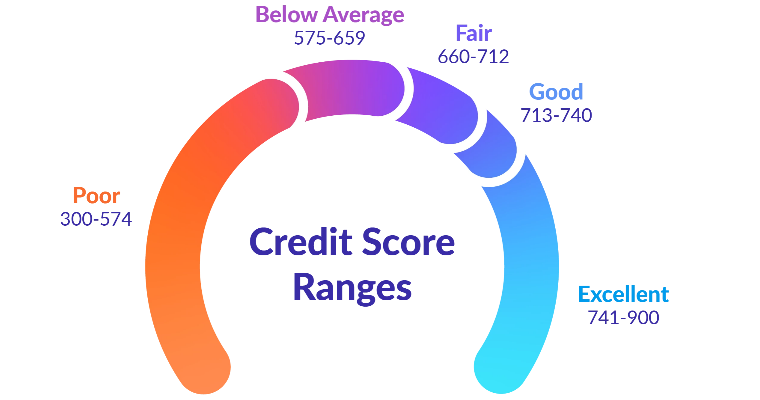

At the heart of this evaluation process lies a specific numerical indicator that reflects an individual’s financial behavior over time. This figure incorporates various elements, including payment history, debt levels, and overall credit utilization. Each part of the equation is vital, contributing to a portrait of reliability that lenders consider when making important decisions.

While many of us may have heard of this term, the intricacies behind it remain a mystery to many. Understanding the components and factors that influence this numerical assessment can empower individuals to take control of their financial futures. With the right knowledge, anyone can improve their standing and unlock better opportunities in the marketplace.

Understanding the Basics of Credit Scores

Getting familiar with the essentials of financial ratings is crucial for anyone looking to navigate the world of borrowing and lending. These evaluations play an important role in decision-making for lenders, influencing everything from loan approvals to interest rates. It’s all about assessing reliability and understanding risk when extending funds to individuals.

The foundation of these ratings typically rests on several key factors, each contributing to the overall assessment. For instance, your history of repayments, the duration of your borrowing relationships, and the diversity of your financial accounts all play significant roles. A strong command over these elements can greatly enhance your standing.

Additionally, it’s vital to remember that certain actions can positively or negatively affect your evaluation. Making timely payments, maintaining low balances on revolving accounts, and regularly monitoring your financial standing are all practical steps to consider. Staying proactive can lead to a favorable impression in the eyes of potential lenders.

Ultimately, grasping the basics doesn’t just equip you with knowledge; it empowers you to make informed decisions, ensuring you’re always on the right track towards financial wellness. Embracing this understanding can open doors to more favorable opportunities in your financial journey.

Factors Influencing Your Credit Rating

Your overall financial reputation is shaped by a variety of elements. Understanding these aspects can be key to maintaining a healthy standing. Let’s dive into the main contributors that can impact how lenders perceive your financial behavior.

Payment history stands out as the most significant element. Regular, timely settlements of bills and loans reassure lenders that you are reliable. On the flip side, missed or late payments can seriously hurt your standing.

Next up, the amounts owed are crucial as well. This refers to the total debt compared to available credit limits. Keeping this ratio low shows that you’re not overly reliant on borrowed money, which is generally viewed positively.

Length of credit history also plays a role. The longer you’ve been managing accounts, the more data lenders have to assess your habits. Older accounts generally provide more stability to your profile.

Types of credit you hold can influence your reputation too. A mix of revolving accounts, like credit cards, and installment loans, such as mortgages or car loans, signals to lenders that you can handle different types of debt effectively.

Lastly, new inquiries can have a temporary negative effect. Each time you apply for new credit, a check is made, which can indicate increased risk if done too frequently. Balancing new accounts while managing existing ones can help keep your standing healthy.

The Impact of Credit Ratings on Loans

Your history of borrowing and repayment plays a significant role in determining the terms and availability of financial assistance. Lenders closely examine this history to assess the likelihood of repayment and decide whether to approve an application. Consequently, maintaining a positive record can open doors to better options and lower interest rates.

When seeking funding, individuals with a strong background often enjoy competitive advantages. They may receive higher amounts and more favorable repayment conditions, allowing them to manage their finances more effectively. In contrast, those with less favorable records may face steeper rates and stricter limitations, which can make it harder to secure the necessary help.

Additionally, the perception of reliability in borrowing influences the overall financial landscape. It can affect not just loan availability, but also insurance premiums and rental opportunities. Thus, understanding the importance of maintaining a strong financial reputation can lead to greater financial freedom and security in the long run.