Understanding the Factors That Can Cause Your Credit Score to Decrease

Many individuals find themselves in a predicament when it comes to their financial standing. A variety of elements can influence how institutions assess one’s reliability in handling borrowed funds. It’s essential to comprehend the nuances that may lead to fluctuations in this assessment. After all, a seemingly minor action can sometimes yield significant changes.

As we navigate through the complexities of financial health, it becomes evident that certain behaviors or choices can impact the overall evaluation from lenders. Every aspect, from payment history to overall debt load, plays a crucial role. Understanding what affects this evaluation can help individuals make informed financial decisions.

It’s worthwhile to explore the common misconceptions and real factors at play. This exploration not only demystifies the process but also empowers individuals to take control of their financial narrative. A clearer insight into how various actions can lead to alterations in one’s financial reputation is crucial for fostering better habits and improving overall stability.

Factors That Impact Your Credit Score

Understanding what can affect financial health is crucial. Many elements play a role in shaping this aspect of personal finance. When evaluating this system, various behaviors and actions come into play, each contributing differently to overall assessments.

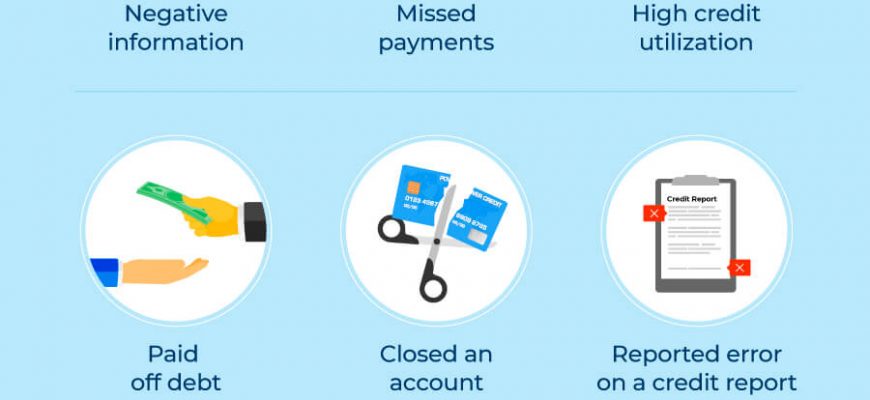

Payment History: This is perhaps the most significant factor. Consistently meeting payment obligations on time demonstrates reliability, while missed or late payments can have a substantial negative impact.

Credit Utilization: The ratio of available credit to the amount being used matters. High utilization can signal risk, while lower utilization often reflects responsible management.

Length of Credit History: A longer history typically indicates experience with managing borrowed funds. Relying solely on new accounts may raise concerns for lenders, as it suggests a lack of established behavior.

Types of Credit: Diversity in the types of accounts held–such as revolving credit lines and installment loans–can positively influence assessments. A wide range shows the ability to manage different financial products.

New Credit Requests: Frequent inquiries for new lines can be seen as a red flag. While a few inquiries every now and then are typically acceptable, too many within a short time frame can signal potential financial distress.

All these components combine to create a comprehensive picture. Recognizing and managing these factors can help individuals maintain a favorable standing in the financial landscape.

Common Misconceptions About Credit Ratings

Many individuals hold misunderstandings about how financial assessments work. These myths can lead to unnecessary worry or misguided decisions. It’s essential to clear up these misconceptions for clarity on how these evaluations truly function and what impacts them.

One prevalent belief is that simply checking one’s financial assessment will have a negative impact. In reality, checking your own assessment is considered a “soft inquiry” and does not affect it at all. This information can be vital for keeping track of financial health without worry.

Another frequent notion is that closing old accounts will always improve financial evaluations. However, in many cases, reducing the length of financial history can inadvertently hurt one’s overall rating. Longer histories often work in favor of individuals, showcasing their reliability over time.

A common error is assuming that personal information, like age or gender, plays a role in financial evaluations. Assessments are strictly based on financial behavior and history, allowing for objectivity in how individuals are rated.

Lastly, there’s a misconception that high income guarantees good evaluations. While income is relevant to financial stability, the determination is mainly focused on how one manages debt and payment history. Responsible financial habits are paramount regardless of income level.

How to Improve Your Financial Rating

Improving one’s financial standing is all about making smart choices and adopting good habits. Whether you’re looking to secure a loan or rent an apartment, understanding the nuances of this evaluation can significantly enhance your prospects. Let’s explore some effective strategies to elevate that number.

First and foremost, paying bills on time is crucial. Late payments can have a long-lasting negative effect. Setting up reminders or automatic payments can save you from those pesky late fees and support a positive financial narrative.

Next, keep an eye on credit utilization. Ideally, it’s best to use no more than 30% of available credit. If possible, try to lower this ratio, as it showcases responsibility in managing borrowed funds. Consider paying off balances more frequently to keep that percentage low.

Additionally, assess existing accounts. Closing old or unused accounts might seem like a good idea, but it can actually minimize your overall available credit and negatively impact your profile. Instead, focus on maintaining those accounts, as they contribute to a healthy credit history.

More importantly, routinely checking reports for errors is vital. Mistakes can happen, and disputing inaccuracies can lead to improvements. Requesting a report annually is a smart move to ensure everything is up to date.

Finally, diversifying types of credit can work in your favor. Having a mix of installment loans and revolving credit can demonstrate broader financial management skills. Just be sure to take on new responsibilities wisely to avoid overwhelming yourself.