Exploring Whether Credit Karma Utilizes FICO Scores in Its Services

Navigating the world of personal finances can feel like walking through a maze. With so many terms and concepts floating around, knowing where to turn for reliable information is crucial. One key aspect many people want to grasp is the system that helps determine their financial standing. This assessment plays a significant role in loan approvals and interest rates, affecting everyday life for many individuals.

There are various tools and platforms available today, each offering insights into one’s financial health. However, not all of them rely on the same methodologies. Some may seem familiar due to their widespread use, while others might introduce alternative approaches to calculate and present scores. Understanding the nuances behind these services is essential for anyone keen on maintaining or improving their financial situation.

In this article, we’ll dive deeper into the specifics of how different services measure financial reliability. By exploring the differences and similarities, you’ll gain a clearer picture of where your information comes from and how to interpret it effectively. Let’s unravel the complexities together!

Understanding Credit Karma’s Scoring Model

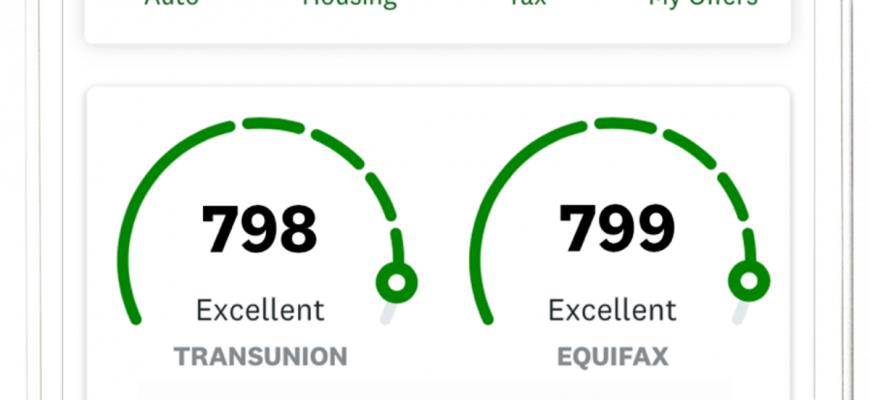

When it comes to assessing your financial health, there are various metrics and models that come into play. One popular platform provides users with insights into their financial standing, helping them make informed decisions regarding their creditworthiness. But what exactly is the scoring method employed by this service, and how does it compare to traditional assessments?

This platform primarily utilizes a version of a scoring model that differs slightly from the conventional standards. Instead of solely relying on the widely recognized scoring system, it presents an alternative view that may help users understand their credit in a different light. This approach focuses on several key factors, including payment history, credit utilization, and the length of credit accounts.

Moreover, the scoring method also emphasizes educational elements, guiding users to improve their scores over time. You won’t just see a number; you’ll also receive tips and personalized recommendations tailored to your unique situation. This empowers individuals to take control of their financial futures, making informed choices to boost their scores.

In summary, while the scoring framework may not align perfectly with traditional metrics, it offers valuable insights for users looking to enhance their financial profiles. Understanding this model can be a game-changer on your journey toward better credit management.

Differences Between FICO and VantageScore

When it comes to assessing creditworthiness, you might notice that there are different scoring models in play. Two popular systems that often come up are FICO and VantageScore. While they both serve the same primary purpose of helping lenders evaluate potential borrowers, they take distinct approaches in how they calculate scores and what factors they prioritize.

One significant distinction lies in the data used to generate the scores. The first model often relies on a more extensive history of payment behavior and debt management, while the latter places greater emphasis on recent credit activity. This variation can lead to different scores for the same individual depending on which model is in play.

Another point of divergence is how each framework treats various types of credit. FICO may weigh different accounts such as credit cards or loans differently compared to VantageScore. This can result in discrepancies, especially for users with diverse credit portfolios. Understanding these nuances is crucial for anyone looking to improve their standing.

Moreover, the scoring ranges can also differ. While both frameworks typically operate within similar numerical limits, the way they categorize scores can fluctuate, impacting how lenders perceive risk. Awareness of these ranges can significantly shape financial decisions.

Ultimately, recognizing the differences between these two scoring systems helps individuals better navigate their financial journeys. By grasping these fundamental distinctions, you can make informed choices that align with your financial goals.

How This Service Benefits Users

This platform offers a range of features that significantly enhance the financial experience for individuals. By providing tools and insights, it empowers users to make informed decisions regarding their financial health.

- Free Access: Users can obtain reports at no cost, eliminating financial barriers to information.

- Personalized Recommendations: Tailored suggestions help individuals improve their financial standing based on unique situations.

- Score Monitoring: Regular updates allow users to track changes in their scores, making it easier to respond to any fluctuations.

- Educational Resources: A variety of articles and tips support users in understanding credit scores and improving their financial knowledge.

Overall, this tool serves as a valuable ally in navigating the complexities of personal finance.