Exploring the Impact of Preapproval on Your Credit Score and Financial Health

When navigating the world of loans and financing, many individuals find themselves pondering the consequences of seeking preliminary assessments from lenders. This topic often stirs a mix of curiosity and concern, leading to questions about how such inquiries can shape one’s financial standing. Getting clarity on this matter is essential for anyone aiming to make informed decisions on borrowing.

While seeking these initial assessments can be a smart strategic move, it’s crucial to understand the potential implications for one’s overall financial profile. Different types of inquiries can have varying effects, and distinguishing between them is key to maintaining a healthy financial situation. The nuances of how each action influences one’s overall metrics can often be overlooked, but they deserve a closer look.

In the end, being well-informed about the processes involved and their potential outcomes will empower individuals to approach their financial journeys with confidence. Issues surrounding the influence of these assessments are often shrouded in confusion, but peeling back the layers can reveal a clearer picture of what to expect. So, let’s dive into the details and uncover the realities involved.

Understanding Preapproval and Credit Impact

When considering borrowing options, many people wonder about the effects of early evaluations on their financial scores. It’s a common concern whether such assessments might lead to a dip in one’s overall standing. Let’s explore how these evaluations work and what they mean for your financial profile.

Initial evaluations are often performed by lenders to determine eligibility for loans or credit products. They help provide insight into the borrowing potential of an individual without requiring a full application. However, the key aspect to keep in mind is the way these evaluations are conducted.

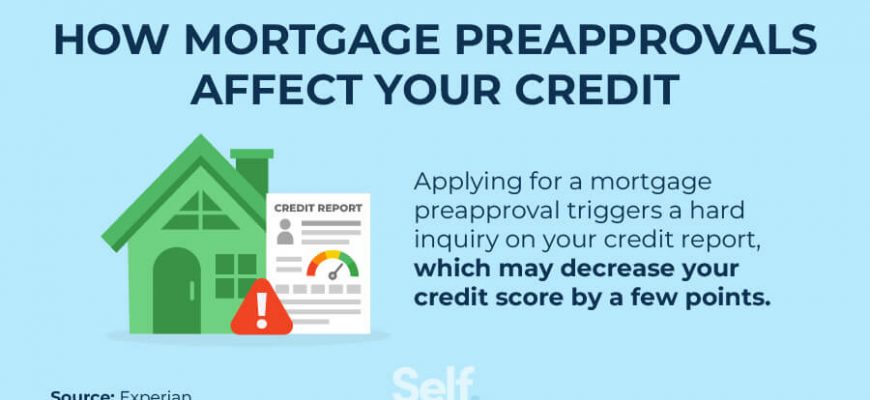

There are typically two types of inquiries: soft and hard. Soft inquiries do not impact your financial standing at all and are often used for background checks or when you check your own score. On the other hand, hard inquiries can lead to a minor reduction in your score, as they indicate that you are actively seeking new credit. It’s important to limit these to avoid unnecessary impacts on your score.

Ultimately, understanding how these evaluations function can empower you to make informed decisions about your financial journey. Keeping an eye on the types of inquiries made and being strategic about when to apply for loans can help maintain a healthy financial profile.

How Preapproval Affects Your Credit Score

When you’re looking to secure a loan or a mortgage, you might wonder how the process impacts your credit standing. It’s important to know that certain actions during this phase can have specific effects on your overall financial profile. Understanding these elements can help you make informed choices as you navigate the landscape of potential lenders and agreements.

One significant factor to consider is the type of inquiry made by lenders. If they perform a hard inquiry, it can lead to a temporary dip in your financial rating. This type of evaluation occurs when a lender reviews your full history to determine your qualifications for borrowing. While it can influence your score slightly, such effects typically fade over time, especially if you manage your other financial behaviors well.

On the other hand, if you engage in multiple assessments within a short time frame, they may be treated as a single inquiry. This practice is designed to allow consumers to shop around for the best deals without severely penalizing their ratings. Thus, being strategic about how often you apply can be beneficial.

Overall, keeping track of various interactions with financial institutions can help you maintain a stable monetary foundation. As long as you are prudent with your applications and payments, the influence of these evaluations can be minor in the grand scheme of your financial journey.

Benefits of Seeking Preapproval Before Loans

Exploring the initial steps before obtaining financing can be incredibly advantageous for potential borrowers. Understanding the possibilities available can empower individuals to make sound decisions regarding their financial futures. When you familiarize yourself with your options ahead of time, it leads to a more informed and confident approach throughout the lending process.

First and foremost, knowing your borrowing potential can simplify the decision-making experience. By securing initial authorization, you gain insight into how much you can afford, which enables you to focus on properties or products that fit within your budget. This clarity can save time and reduce frustration while searching for the right fit.

Additionally, having initial backing from lenders places you in a stronger position when negotiating terms. Sellers and lenders often view individuals with prior approval as more credible and serious contenders, providing an edge in competitive markets. This perceived reliability can lead to more favorable terms and conditions.

Lastly, going through this process can reveal areas for improvement within your financial profile. It provides an opportunity to identify and address any outstanding issues, enabling you to enhance your financial standing. This proactive approach can lead to better rates and options when the time comes to secure funds.

In essence, taking the time to engage in this preparatory step not only clarifies your financial landscape but also fosters confidence and enhances your negotiating power when pursuing loans.