Exploring the Landscape of Credit Risk in Europe and Its Impact on Financial Stability

In the dynamic landscape of financial transactions, a multitude of factors contribute to the potential challenges associated with lending and investment activities. Understanding the delicate balance between opportunity and the unforeseeable complications is essential for both institutions and individuals. This exploration delves into the nuances of monetary engagements and the factors that can influence the stability of these essential operations.

The environment for monetary dealings is ever-evolving, shaped by various elements such as economic trends, consumer behavior, and global happenings. These influences can create fluctuations that seem unpredictable at first glance, yet often follow recognizable patterns. Navigating this complex terrain requires a keen awareness of both the promising avenues for growth and the potential pitfalls that lurk beneath the surface.

As we dissect the intricacies of this financial domain, we reveal insights that can aid in making informed decisions. By identifying the various stimuli that play a role in shaping financial scenarios, stakeholders can better position themselves to handle uncertainties and foster a more secure economic future.

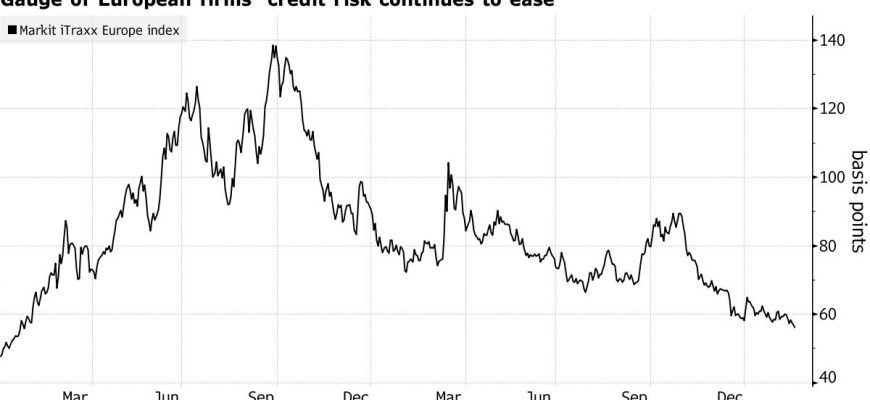

Understanding Financial Vulnerability in Europe

When we delve into the world of lending and borrowing across the continent, we encounter various intricacies that impact both institutions and individuals. It’s essential to grasp how these financial interactions shape economies and influence decision-making processes. Various factors play a role in determining the stability of these transactions, reflecting a complex tapestry of relationships that are critical to navigating this landscape.

The financial environment here is characterized by diverse markets, regulatory frameworks, and varying economic conditions. Institutions must continually assess potential pitfalls that could affect their engagements with clients. Understanding the underlying determinants, such as macroeconomic indicators, consumer behavior, and geopolitical factors, can provide a clearer picture of the challenges faced by lenders and borrowers alike.

Moreover, evaluating not just the present but also the anticipated future scenarios is vital. This involves analyzing trends and shifts that may influence the ability of individuals and organizations to meet their obligations. With advancements in technology and data analytics, stakeholders are better equipped to make informed choices, reducing the possibility of unfavorable outcomes.

Awareness and education play a significant role in this arena. By enhancing understanding among individuals and entity leaders about the nuances of lending, they can better position themselves to handle potential challenges. Fostering a culture of openness and transparency will ultimately benefit the entire financial ecosystem, creating more secure and reliable partnerships.

Factors Influencing Financial Assessment

When assessing the potential for default, there are several elements that come into play, shaping the overall picture of an individual or entity’s ability to meet financial obligations. Understanding these aspects is vital for making informed decisions in lending and investment. From economic indicators to personal circumstances, the nuances of each variable can significantly impact evaluations.

One of the primary components is the economic landscape, including growth rates, unemployment levels, and inflation. A thriving economy can boost confidence and repayment abilities, while downturns can raise concerns. Additionally, an individual’s credit history plays a crucial role; previous behavior regarding borrowing and repayments offers insights into future actions. A clean slate can be quite appealing, whereas a checkered past might raise some eyebrows.

Another factor to consider is the financial stability of the borrower. Income levels, job security, and assets are key indicators of one’s capacity to honor commitments. Moreover, industry trends can also affect assessments, as some sectors may face more volatility than others. Staying informed about these trends can provide context and influence judgment.

Lastly, external factors such as regulatory changes and geopolitical events can alter the landscape. Keeping an eye on these dynamics helps in developing a more rounded view of the situation. In essence, evaluating potential shortfalls is a multifaceted process that requires careful consideration of various influences.

Strategies for Mitigating Financial Exposure

In today’s financial landscape, managing potential negative outcomes is crucial for long-term stability. Organizations need to adopt comprehensive approaches to navigate uncertainties associated with lending and investment. By implementing effective strategies, they can safeguard their interests and ensure sustainable growth.

One of the primary methods involves thorough assessment and analysis. By conducting in-depth evaluations of potential borrowers, businesses can gain insights into their financial health, repayment capabilities, and overall reliability. Utilizing advanced algorithms and data analytics tools can further enhance this process, enabling more informed decisions.

Diversification is another essential strategy. Spreading investments across various sectors can significantly reduce the potential impact of any single client’s financial troubles. By not putting all eggs in one basket, businesses can create a more resilient portfolio that can weather economic fluctuations.

Additionally, establishing robust monitoring systems is vital. Regularly reviewing clients’ performance, market conditions, and industry trends helps organizations stay ahead of potential issues. Implementing early-warning systems can signal when intervention might be necessary, allowing companies to act proactively rather than reactively.

Lastly, fostering strong relationships with clients is invaluable. Open communication channels can lead to more transparency and trust, making it easier to navigate difficulties together. When clients feel supported, they are more likely to prioritize their obligations, ultimately benefiting both parties.